Ternary materials are materials that consist of three chemical components (elements), components (elements and compounds) or parts (parts). In the cathode material of a lithium battery, it generally refers to a material having a chemical composition of LiNixXyCozO2. Wherein X is Mn (manganese) is NCM (commonly known as lithium nickel-cobalt-manganese oxide), and X is Al (aluminum) refers to the NCA (commonly known as nickel-cobalt-aluminate).

I. Industry Overview

1. Definition of Sanyuan Material Industry

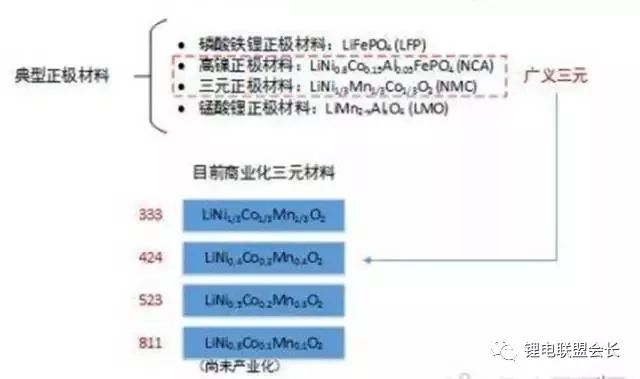

Ternary materials are materials that consist of three chemical components (elements), components (elements and compounds) or parts (parts). In the cathode material of a lithium battery, it generally refers to a material having a chemical composition of LiNixXyCozO2. Wherein X is Mn (manganese) is NCM (commonly known as lithium nickel-cobalt-manganese oxide), and X is Al (aluminum) refers to the NCA (commonly known as nickel-cobalt-aluminate). The so-called 111, 532, 622 and 811 models refer to the ratio of the three numbers of x, y, and z in the NCM material. For example, the x:y:z in 622 equals 6:2:2, and its chemical composition It is LiNi0.6Mn0.2Co0.2O2. From the perspective of the microstructure of the material, NCA and NCM are very similar, but due to the fact that LiNi0.8 Al0.05Co0.15O2, which is currently being used by Panasonic, is currently used for industrial scale manufacturing, the NCA has evolved into a special one. Refers to.

Figure: Typical Lithium Battery Cathode Materials

Both NCM and NCA are essentially to solve the stability problem of lithium cobaltate (LiCoO2) or lithium nickelate (LiNiO2) layered structures. Both manganese and aluminum play a supporting role in them, in which manganese is incorporated. Lithium and nickel layers can be guided to mix, thus improving the high-temperature properties of the material; the incorporation of aluminum can improve the lattice structure of the material to a certain extent, reduce the collapse, and then improve its cycle stability. The two technical routes themselves are not highly divided. Even NCM may have security advantages due to better stability of Mn. The future of the development trend of who is the ternary material depends on who is after the industrialization application. Ni content is higher.

Positive ternary materials and lithium cobalt oxide, lithium manganese oxide, lithium iron phosphate performance comparison:

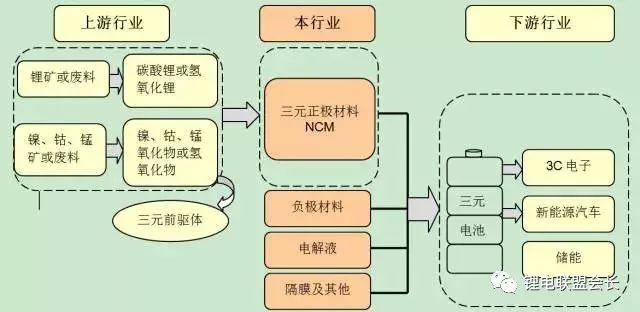

2, ternary materials industry chain diagram

Take ternary battery NCM as an example, the upstream of the industrial chain includes ternary precursors and corresponding mineral resources (lithium, cobalt, manganese, and nickel), and the middle reaches include ternary cathode materials, electrolytes, anode materials, separators, and others. The downstream applications are mainly used in 3C electronics, new energy vehicles, and energy storage batteries [1].

[1] Energy storage battery: It refers to a battery used for solar power generation equipment, wind power generation equipment, and renewable energy storage energy.

Figure: NCM Industry Chain Diagram

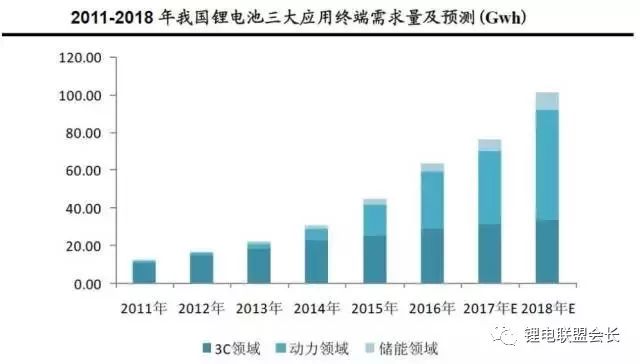

From the perspective of China's lithium battery applications, the rapid development of power, energy storage and 3C industries has become the main driving force for the development of lithium-ion battery industry, and the demand for lithium batteries in the field of power and energy storage is accelerating.

1) 3C is still the main downstream consumer terminal of lithium-ion batteries, but the growth rate has gradually begun to slow down, and the use of three-cell batteries in the 3C field is relatively small, mainly lithium cobalt oxide batteries;

2) The rapid development of the new energy automotive market, power lithium battery has become the main support for the positive material market, an obvious increase. As the mainstream development direction of the future power battery, Sanyuan Battery will directly benefit from the rapid growth of the new energy vehicle market and the major growth point of future ternary material demand;

3) Energy storage is poised for growth and room for growth is about to open. It is predicted that the market demand for lithium battery cathode materials in the energy storage sector will exceed 40% annually during 2015-2018.

3, the development status of the ternary materials industry

3.1 Overview of the Sanyuan Material Market

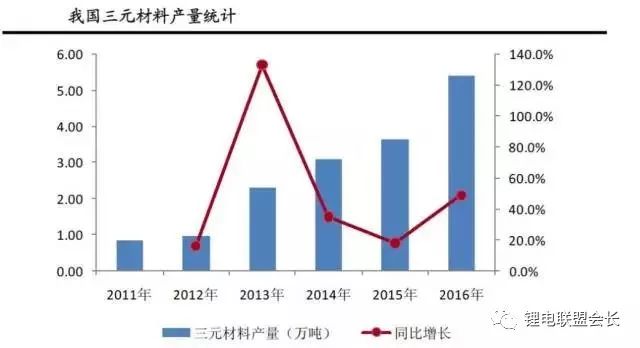

Due to the rapid growth of downstream new energy vehicle production and the steady growth of 3C electronic product shipments, the output and output value of cathode materials in China have shown a rapid growth. In 2016, China's lithium battery cathode material production was 161,600 tons, an increase of 43.14% year-on-year; from 2010 to 2016, the compound annual growth rate was as high as 36.48%. The industry output value increased from 5.7 billion yuan in 2010 to 20.8 billion yuan in 2016, with a compound annual growth rate of 24.08%.

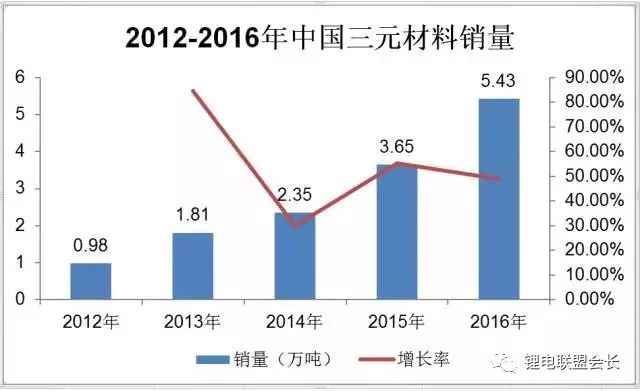

Supported by the rapid development of power lithium batteries, ternary materials have shown rapid development momentum. Affected by the demand of the downstream power market, new high-voltage cathode materials and high-nickel ternary materials have begun to receive attention from manufacturers, R&D efforts have increased, and Began to market. According to statistics, in 2016, the output of lithium ternary materials in China was 54,300 tons, a year-on-year increase of 48.8%; the output value was 7.98 billion yuan, which was a year-on-year increase of more than 60%. Among the four types of cathode materials, the output value accounted for the highest proportion.

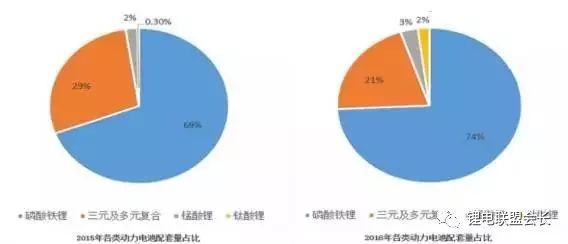

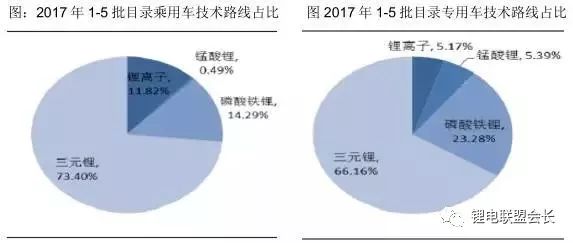

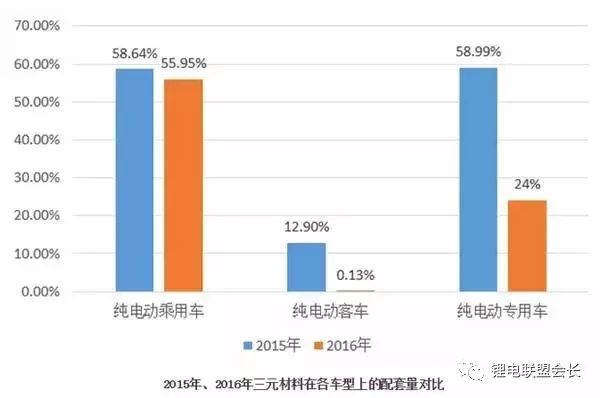

In 2016, due to the government's suspension of the inclusion of ternary lithium battery passenger cars in the promotion of new energy vehicles, 2016, Sanyuan’s battery capacity decreased by 8% compared to 2015, mainly due to the application of Sanyuan’s battery in pure electric vehicles. The decrease shows that in 2016, the proportion of ternary material batteries in special vehicles fell from 58.99% to 24%, and the proportion of lithium iron phosphate batteries increased from 36.25% to 71.12%. With the renewal of the ternary battery at the bus, the outstanding advantages of Sanyuan Battery are even more obvious, especially in the fields of passenger cars and special vehicles. In the 1-5 batch of new energy vehicle promotion catalogue in 2017, passenger cars and special vehicles Yuan accounted for more than 70%.

Chart: Comparing the proportion of power batteries in 2015 and 2016

3.2 Ternary Material Technical Route

At present, the ternary cathode material mainly includes two technical routes, namely, an NCM route using lithium nickel-cobalt-manganese oxide as a positive electrode and an NCA route using lithium nickel-cobalt-aluminate as a positive electrode. Both NCM and NCA are essentially to solve the problem of the stability of lithium cobaltate (LiCoO2) or lithium nickelate (LiNiO2) layered structures. Manganese and aluminum play a supporting role in both of them. limited. The incorporation of manganese can guide the mixing of lithium and nickel layers, thus improving the high temperature performance of the material; the incorporation of aluminum can improve the lattice structure of the material to a certain extent, reduce the collapse, and then improve its cycle stability.

(1) Nickel cobalt manganese oxide (NCM)

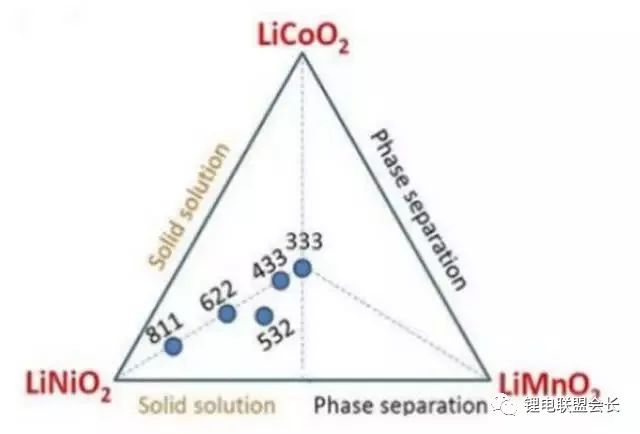

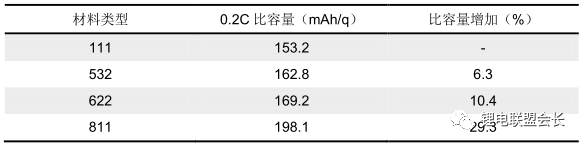

According to the composition, NCM can be divided into two basic series: low-cobalt symmetric ternary materials and high-nickel ternary materials. The former has a Ni/Mn molar ratio of 1 fixed to maintain the valence balance of the ternary transition metal oxide. Representative products are 333 and 442 ternary materials. Due to the lower Ni content, this type of material has a relatively high Mn content and a relatively complete crystal structure, and therefore has the potential to develop at high pressures; the high-nickel ternary material uses a hydroxide co-precipitation process to make Ni, Co, and Mn three elements in the precursor. The homogeneous distribution at the atomic scale is achieved. The currently representative components of the high nickel ternary are 622, 701, 515, and 811. The physical properties of the 811 are very similar to those of the NCA. The actual g capacity in a full cell can be over 190 mAh/g.

Although increasing the nickel content can increase capacity, the negative effects are equally evident. With the increase of nickel content, the effect of mixing and evacuation of Ni in the Li layer is also more obvious, which will directly deteriorate its cycle performance and rate performance [2]. Moreover, increasing the nickel content makes the stability of the crystal mechanism worse, and the surface residual alkali content also increases, these factors will lead to more prominent safety issues, especially in the high temperature test conditions, the battery core gas production is very serious.

[2] Rate performance: refers to the battery discharge performance under different charge and discharge currents.

The technical difficulty of high-nickel industrialization lies in the production of precursors, the sintering of products, and the surface treatment processes. The technical content of ternary materials is 60% in the preparation process of precursors. Precursor preparation must strictly control the atmosphere and the concentration of the complexing agent, otherwise the nickel content will deviate from the stoichiometric ratio, resulting in a higher precursor carbon content, and the precursor quality (morphology, particle size, particle size distribution, specific surface area, impurities The content, tap density, etc.) directly determine the physicochemical index of the final sintered product; the sintering process is mainly embodied in the selection of the dopant, the temperature of the sintering process and the control of the atmosphere.

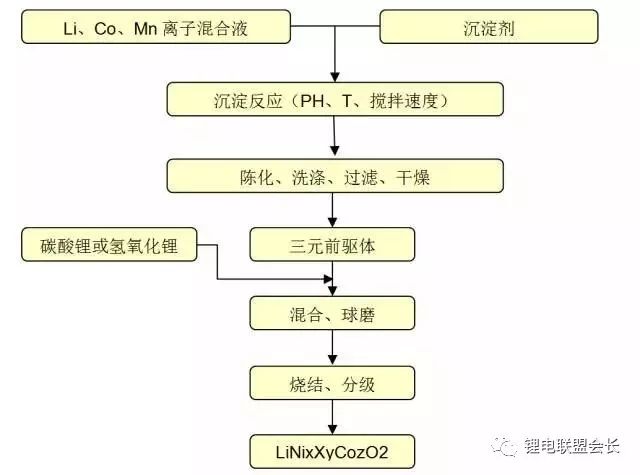

NCM production process:

(2) Lithium Nickel Cobalt Aluminate (NCA)

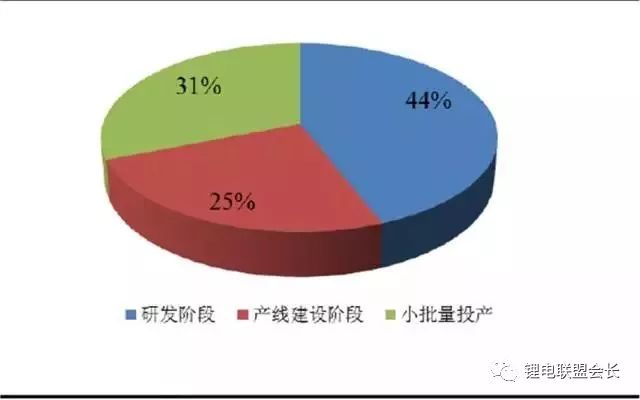

The ternary NCA materials started earlier in foreign countries and started later in the country. According to statistics of GGII, as of the end of 2016, there were more than 15 companies engaged in NCA production in China, most of them were in the early stage of construction and development, and a small number of companies were in the stage of sample testing for small batch production. There was a clear gap between Japan and South Korea. Currently, Tesla's electric vehicles use NCA batteries for Panasonic in Japan, driving the global NCA production boom. At present, the domestic NCA production volume is about several hundred tons.

Figure: Progress of domestic NCA material companies at the end of 2016

The difficulty of industrial production technology of NCA materials lies in the need to master the coprecipitation process of the precursor first, followed by the need for unique Al doping technology, and the sintering process temperature and atmosphere control is also high. In addition to material factors, the battery production process also needs to be matched with the NCA material. The NCA material is very easy to absorb moisture due to the high content of alkaline substances on the surface. Therefore, it is required that the homogenization coating plant must control the moisture very strictly in order to prevent In the process of homogenization, the slurry tends to form a jelly, which can not be coated. In addition, special measures must be taken during the homogenization process to improve the coagulation of the slurry than adding a small amount of oxalic acid. Panasonic Corporation also added one to NMP. A special co-solvent to improve agglomeration during the beating process. In addition, there is a higher requirement for the matching of the electrolyte with NCA. Otherwise, the battery air inflation will be severe and the high temperature cycle and storage will be difficult to pass.

4. Future development trend of ternary materials

Technology tends to be high-nickel: The increase in the content of nickel in ternary materials will increase the capacity of materials, and the overall performance will be greatly affected by the ratio of nickel, cobalt and manganese. In the future, the demand for battery energy density will continuously increase. Metamaterials will develop towards high nickelization. However, considering that the increase in nickel content will affect the structural stability, thermal stability, and cycle performance of the product, the trend of high nickelization will further test the ability of the company to control the product.

Table: Specific capacity of different types of NCM materials

Increased industry concentration and more intense competition at mid-to-low-end: The Ministry of Industry and Information Technology launched the “Regulatory Conditions for Automotive Power Battery Industry†in 2016 (draft for solicitation of opinions), and proposed a basic requirement of 8GWh per year for downstream battery companies, compared to the original The demand has increased by 40 times. This policy will greatly promote the concentration of industries. Lithium iron phosphate and ternary materials companies related to power batteries have launched expansion plans and exacerbated the industry's reshuffle. At the same time, with the large-scale effect, the battery cost of power battery companies will decline, which will certainly impact the upstream cathode material company's cost, and require cathode material companies to meet the requirements of power battery companies for higher performance materials. It is expected that there will be a price war in the future. The overcapacity of low- and medium-end positive electrode materials will lead to higher-tech leading companies that can meet the demand of higher-performance materials for power battery companies. The market concentration will be further enhanced, and the strong will be displayed.

Second demand side analysis

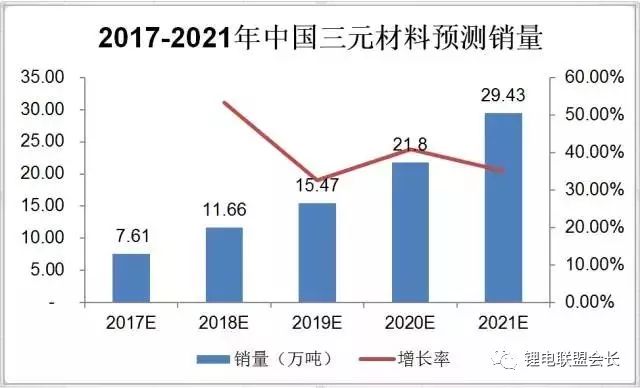

1. Market volume data analysis in the past five years

Benefiting from the rapid growth of domestic electric vehicle power batteries, cobalt substitution of 3C batteries, electric tools, and electric bicycles, the demand for China's ternary materials market has continued to grow rapidly. In 2016, the size and sales volume of China's ternary materials market reached 7.98 billion yuan and 54,300 tons, respectively, an increase of 68% and 49% year-on-year respectively in 2015.

The increase in output of the Sanyuan battery market was mainly driven by new energy passenger vehicles, lithium-powered bicycles, and low-end digital lithium batteries. The increase in market output value over production was mainly due to the following reasons:

a) In 2016, the power battery of new energy vehicles maintained rapid growth, and the demand for passenger cars for ternary materials accelerated; b) The prices of nickel and cobalt metals showed an upward trend throughout the year, of which nickel metal prices rose by more than 20,000 yuan year-on-year at the beginning of the year RMB/ton, cobalt metal rose by more than 60,000/ton, thus driving up the price of ternary precursors and finished materials; c) High-nickel materials such as 622, 811 and NCA gradually released their production capacity and formed sales, and their prices were higher than the conventional model 532 More than RMB 15,000/tonne, it will drive the increase in total output value; d) The price of lithium cobaltate will increase sharply in the second half of 2016. Some digital battery companies will use ternary materials instead of cobalt acid in order to save costs. lithium.

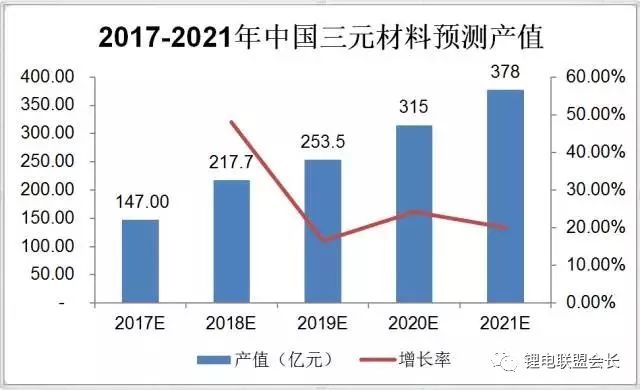

2. Forecast Market Data Analysis in the Next 5 Years

In 2016, China's new energy vehicles were in the period of policy adjustment, and were affected by policies such as inventory deception, temporary suspension of three-cell batteries for commercial vehicles, battery catalogs, adjustment of subsidy policies, delayed release of recommended catalogs of pure electric logistics vehicles, and growth of new energy vehicles 36.41. %, lower than expected at the beginning of the year. However, from a global perspective, China’s new energy vehicle market is still the fastest growing market in the world. According to the latest requirements of the Ministry of Industry and Information Technology, since Jan. 1, 2017, the application of Sanyuan Battery in passenger vehicles has been lifted, and Sanyuan Materials is expected to maintain rapid growth.

In 2021, the domestic ternary materials market is expected to reach 37.8 billion yuan, a compound annual growth rate of 36.49%, mainly due to the growth in demand for power batteries. Policies to promote ternary materials have become the only way, according to the "promote the automotive power battery industry development action plan", by 2025, the new system power battery technology made a breakthrough, the monomer specific energy of 500 watt hours / kg. At present, Sanyuan is the most likely technical route to meet relevant requirements. According to the forecast of the industry information network, Sanyuan Materials will account for half of the total output of lithium iron phosphate in 2019, and the ternary materials market will account for more than 55% in 2020.

3, the overall situation of market demand

In terms of pure electric passenger vehicles, Sanyuan still holds a dominant position, accounting for 55.95% in 2016. Although the proportion decreased by 2.7% compared to that of 2015, its supporting volume has quadrupled to 4.65GWh.

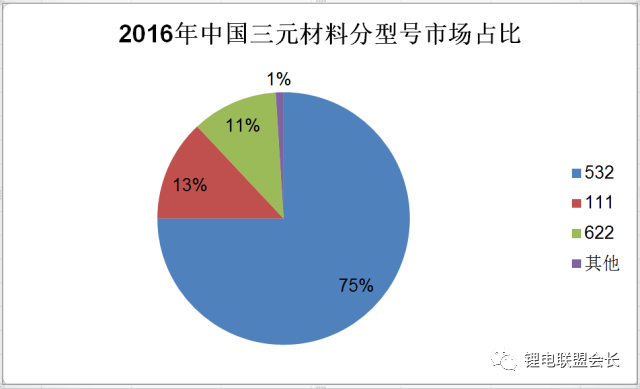

The domestic ternary material model is mainly 532, and 532 ternary material, originally developed by Samsung SDI to circumvent the US 3M patent, has become the best-selling ternary material on the market. From the battery shape point of view, the domestic cylindrical ternary battery commonly used NCM532, the use of laminate technology ternary power battery using NCM111, which ternary cylinder output is greater than the square laminated battery.

4, the main demanders and characteristics

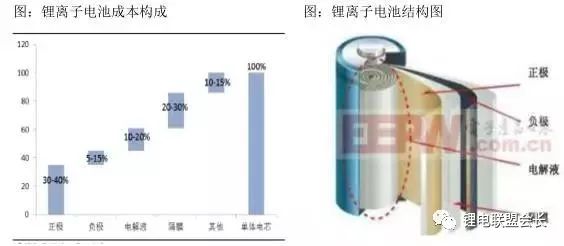

The core structure of the lithium-ion battery cell includes a positive electrode material, a negative electrode material, an electrolyte, and a separator. Specifically, the cathode material accounts for the largest proportion in the manufacturing cost and quality of the cell, which directly determines the safety and energy density of the power cell product.

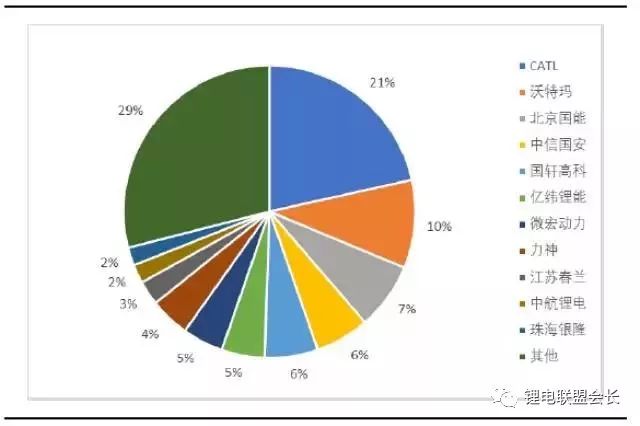

The concentration of the power lithium battery industry has increased significantly: The Ministry of Industry and Information Technology has successively published the 292th to 297th batches of road vehicles and production enterprises and products. There are 1,743 new energy vehicles in the catalogue. Among the top five battery companies, the number of models supported exceeds 50% of the total. The vast majority of models are concentrated in CATL, Waterma, Beijing Guoneng, CITIC Guoan and Guoxuan Hi-Tech, among which CATL comes in each batch of this year. The number of car models in the catalogue is the first, and the number of CATL models in the field of passenger cars and passenger cars is the first. In the special car category, the number of the models for Watermark, Beijing National Energy and CATL is mostly.

Figure: The recommended number of matching models

The pace of expansion of battery manufacturers is firm: According to public information, battery manufacturers have a clear capacity plan. Currently, the four major capacity battery manufacturers are BYD, CATL, Waterma, and Guoxuan Hi-Tech. The 2016 lithium battery capacity of the four companies totals 35.5GWh. BYD's capacity planning for 2020 will reach 34GWh. CATL plans to have a capacity of 50GWh by 2020. The battery plant capacity planning is as follows:

Table: Capacity Planning for Major Battery Manufacturers

Lithium battery overcapacity promotes industry reshuffle: According to domestic production and sales of new energy vehicles in 2017-2018, domestic demand for lithium iron phosphate batteries is 16GWh and 18GWh in China in 2017-2018, and demand for lithium battery in ternary materials is 14GWh. And 24GWh, while domestic lithium iron phosphate battery capacity has reached 63GWh, Sanyuan battery capacity has reached 39GWh, from the supply and demand structure, the current lithium battery industry is in a state of excess capacity.

Overcapacity will accelerate the industry's reshuffle.

1) The energy density requirement of lithium iron phosphate battery is increased, and backward production capacity is eliminated. Enterprises with scale, technological advantages and financial strength survive;

2) The expansion of lithium iron phosphate production capacity has slowed down, and some companies have gradually switched the capacity of some lithium iron phosphate batteries to triple battery capacity (a production company with a mature ternary battery technology may require that the production line be adjusted from lithium iron phosphate to three yuan. Months or so, but the capacity switching may take 2-3 years for companies without prior ternary battery production technology experience. At the same time, the battery specifications and model are different, and not all production lines can be directly switched;

3) Leading lithium battery companies continue to invest in the construction of three yuan battery capacity, while the technical path to the development of high density three yuan lithium battery, such as NCM (622,811) and NCA.

Major manufacturers: According to the "2016 China New Energy Vehicle Market Report" co-launched by the 21st Century Business Herald and Wilson Consulting Co., Ltd., the domestic power battery market shipments reached 28.04Gwh in 2016, and ternary battery shipments accounted for Compared with 31%, Ningde ranked first.

Three supply side analysis

1. Supply situation and main participants

At present, the world's larger ternary materials manufacturers are mainly concentrated in China, Japan and South Korea, and together account for about 50% of the market share. Japan accumulates and controls the market with its unique expertise, and Korean companies have rapidly emerged in recent years. They are highly competitive in terms of technology and product quality. Chinese companies have not been in the company for a long time. Jinrui Technology, which is driven by Tesla, is the first NCA material supplier in China, and other companies have set foot in the tern.

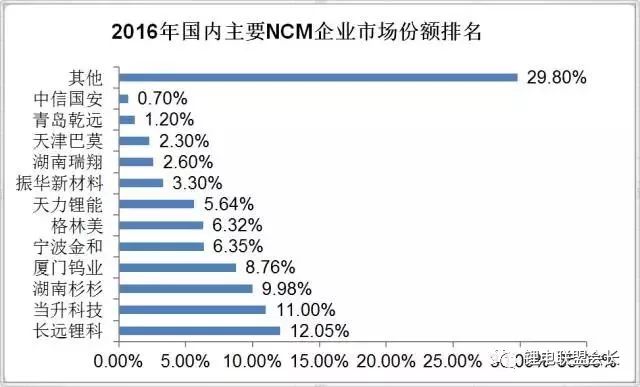

At present, the supply of domestic ternary materials is more concentrated, according to EVTank's ranking of ternary cathode materials company's market share in the report, Long-Term Lithium Branch, Dangsheng Technology, Hunan Shanshan, Xiamen Tungsten Industry, Ningbo Jinhe and the top five companies. The total market share in 2016 reached about 50%, and the market share of the top ten manufacturers in 2016 was about 68%. With the stability and maturity of the ternary battery industry chain, the stability of downstream materials and vehicle companies will be more and more important to the stability and quality of materials supply, as well as the importance of brands. Large companies that have the advantages of technology and capital will compete with small companies that follow the trend. With significant advantages, the overall market share of large companies in the future is expected to maintain or even increase.

According to the current capacity building and planning information released by mainstream domestic manufacturers, only the mainstream manufacturers have exceeded 300,000 tons of capacity for the construction of ternary materials, which is not counting the unreported capacity of small and medium-sized small enterprises. Assume that only 2017 will be only 100%. The 50-to-production capacity has reached a production capacity of 150,000 tons, far exceeding the forecasted demand for ternary materials, and the overcapacity has started to show.

Table: Capacity Planning for Some Domestic Triomaterial Manufacturers

The main participants:

(1) Hunan Shanshan (stock code: 600884.SH)

Hunan Shanshan was established in 1992. It is the first company to enter the lithium-ion battery material market in China. Currently, it is the largest supplier of lithium-ion battery materials in China and the world’s largest integrated production capacity. It is the fourth consecutive year in the IIT General Research Report of Japan. The only Chinese lithium battery maker listed on the list has established strategic partnerships with internationally renowned companies such as Samsung, LG, and Sony. The company's products include lithium battery positive and negative materials, electrolytes and positive electrode material precursors. In 2016, the company's cathode materials achieved sales revenue of RMB 2.5343 billion.

(2) Xiamen Tungsten Industry (stock code: 600549.SH)

Xiamen Tungsten Industry Co., Ltd. was established in 1997 and operates in tungsten, molybdenum, rare earth, new energy materials and real estate industries. After 30 years of development, the tungsten industry has formed a complete tungsten industrial chain from tungsten mines, smelting, deep processing to recycling tungsten secondary resources, of which tungsten filaments for lamps account for more than 50% of the world market share. The rare earth industry has formed a relatively complete industrial system from rare earth mine development, smelting and separation, rare earth functional materials (rare earth permanent magnet materials, energy storage materials, luminescent materials, etc.) and scientific research applications. In the field of new energy materials, lithium-ion positive electrode materials and nickel-metal hydride battery anode materials (hydrogen storage alloys) have been established. Lithium-ion battery cathode materials include lithium cobaltate, ternary materials, lithium manganate and lithium iron phosphate. In 2016, the company's battery materials achieved a sales income of 2,050.51 million yuan.

(3) Tianli lithium energy (stock code: 833757.OC)

Xinxiang Tianli Limnium Co., Ltd. was established in 2009 with a registered capital of 21 million. It is currently the largest domestic manufacturer specializing in R&D, production, and sales of secondary power battery materials. The company's main products are lithium nickel-cobalt-manganese-cobalt-manganese acetate cathode materials for new lithium-ion batteries, with an annual production capacity of 5,000 tons; nickel-metal hydride battery negative electrode hydrogen storage alloy powder product series, with an annual output of 1,000 tons of scale strength; Zinc manganese battery anode material zinc powder product series, with an annual capacity of 3,000 tons of scale. In 2016, the company's ternary materials achieved a sales income of 311.72 million yuan.

(4)Dangsheng Technology (stock code: 300073.SZ)

The company is a Beijing high-tech enterprise engaged in R&D and production of new energy materials. It is mainly engaged in the research and development, production and sales of lithium cobalt oxide, multi-materials, lithium manganese oxide and other small lithium-ion, lithium-ion cathode materials. The company is the first supplier to export lithium cathode materials in China. The top six lithium giants in the world have five customers, including Samsung SDI, LG Chem, Sanyo Energy, Shenzhen BAK and BYD. In 2016, the company's cathode material for lithium battery realized sales income of 1,156.58 million yuan.

2. Supply chain upstream and main participants

The upstream of the industrial chain of ternary materials mainly includes ternary precursors and corresponding mineral resources (lithium, cobalt, nickel, manganese ore, and waste recycling). With the rapid development of the new energy automotive industry, the quantity of cobalt and lithium has increased. The current market is in short supply.

(1) Lithium ore and lithium carbonate

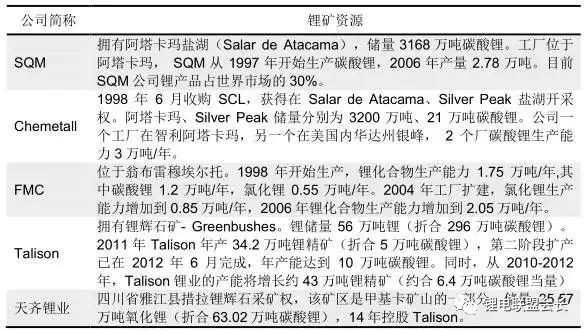

Lithium ore resources are basically monopolized. Before 2014, the five companies controlled 82% of the world's lithium resource supply. Among them, Tianqi Lithium and Lockwood jointly controlled Tellison (the equity of Tianqi Lithium accounted for 51%, and Lockwood shares After accounting for 49%, it is equivalent to controlling about 50% of global lithium resources.

Table: The world's major lithium mine suppliers

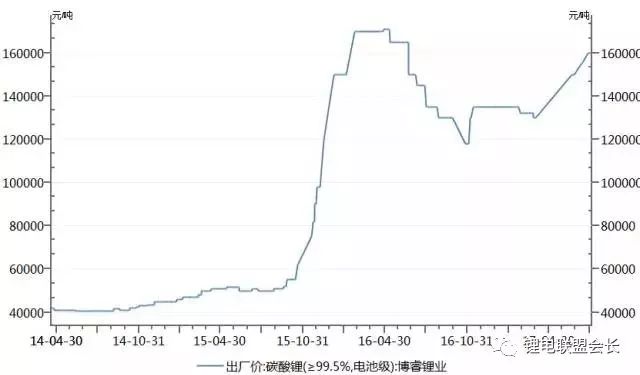

Lithium carbonate is the main raw material for the production of ternary materials. The material cost of lithium carbonate accounts for more than 50% of the cost of the entire ternary materials. The price of lithium carbonate directly determines the cost of ternary materials, and the global supply of lithium carbonate and its derivatives About 70% of the amount comes from the salt lake brine, about 30% from the ore to extract lithium. Although lithium resources are not scarce, lithium resources with economic recoverable value are highly concentrated in the salt lake lithium extraction companies SQM, Rockwood, FMC and spodumene companies Talison, Galaxy hands, so the global pricing power of lithium carbonate is basically concentrated in the above companies . With the increase in the demand for ternary materials for new energy vehicles, especially passenger vehicles, lithium carbonate is in short supply. In 2015, the domestic lithium carbonate supply gap reached 15,000 tons, resulting in the price of lithium carbonate from 14 years. Million/ton rises to the current 160,000/ton.

Chart: 14-16 lithium carbonate price charts

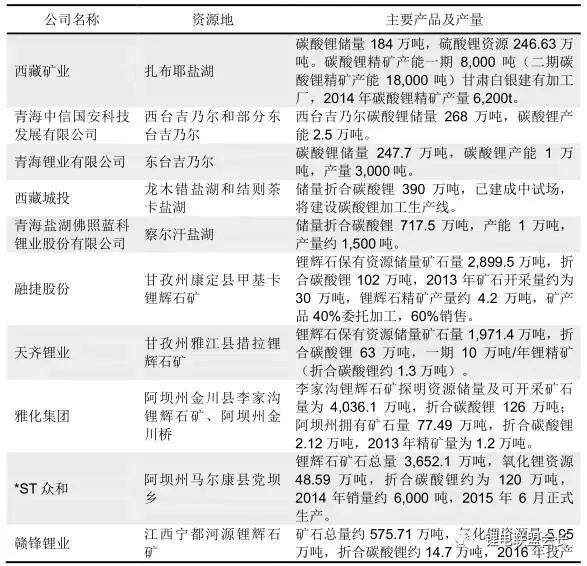

The major domestic lithium resources and production capacity are as follows:

(2) Cobalt

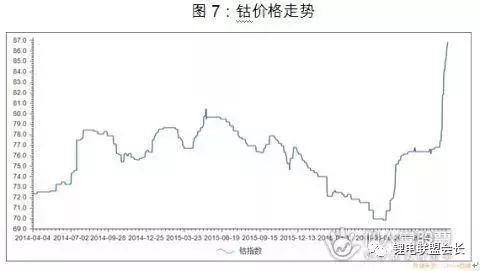

The world’s major cobalt reserves are concentrated in Africa. The largest reserve country is Congo, which accounts for 47% of the world’s total reserves. China’s reserves are extremely small, accounting for only 1.11% of global reserves. However, due to limited production conditions in Africa, such as electricity, cobalt ore is exported to deep processing abroad, of which China is the main cobalt ore deep-processing country, and 42% of the world's cobalt ore is refined in China. Driven by the demand for new energy vehicles, the price of cobalt has bottomed out in the second half of 2016. Since November, the price of cobalt has increased by more than 10%, and the potential for subsequent outbreaks has been greatest. According to a research report issued by Guojin Securities on October 22, 2015, “Strong Demand, Constrained Supply, and Approaching Inflection Point in the Cobalt Market,†it is predicted that from 2015 to 2020, the global supply and demand balance of cobalt will continue to improve and it will emerge in 2016. In short supply, the shortage of cobalt market will increase to 6,600 tons by 2020.

The main cobalt mineral resources in China are as follows:

(1) Jinchuan Group

Jinchuan Group is a world-renowned large-scale non-ferrous metallurgy and chemical joint enterprise engaged in mining, selection and metallurgy. It is the largest nickel-cobalt-platinum group metal production enterprise in China and the third-largest copper producer in China. It conducts non-ferrous metals in 24 countries and regions in the world. Metal mineral resources development and cooperation. Currently, Jinchuan Group currently has 19 mining licenses, 29 exploration licenses, and controlled mineral resource reserves, including approximately 4.35 million tons of nickel, 9.95 million tons of copper, 430,000 tons of cobalt, and 1,110 tons of platinum. The reserves of cobalt metal, reserves of platinum group metals, and reserves of cobalt resources that can be developed and utilized rank first in the country.

(2) GEM (stock code: 002340.SZ)

GEM's acquisition of KARL has also greatly enhanced the development potential of the cobalt industry. The company has obvious advantages in the ultra-fine cobalt powder industry. The company is the largest company in China that uses waste resources to recycle ultra-fine cobalt nickel powder, and it is used internationally for disposal. Cobalt-nickel resources The advanced enterprise producing ultra-fine cobalt-nickel powder materials, and one of the industrial bases for cobalt-nickel powder materials and recycling technology in China. Dedicated to the research and industrialization of the recycling technology industry, adopting secondary resources to produce high-tech materials through recycling technology, and forming ultra-fine cobalt powder, ultra-fine nickel powder, advanced battery materials, and lead-free welding materials using secondary resources such as used batteries. And other products, with resources and cost advantages.

(3) China Metallurgical Corporation (stock code: 601618.SH)

The company is one of the world's largest engineering construction integrated enterprise groups. It is a multi-specialized, cross-industry, and multinationally-operated super-large enterprise group focusing on project contracting, resource development, equipment manufacturing, and real estate development. China National Metallurgical Joint Ventures Jinn Nickel, Jinchuan Group Co., Ltd. and Jiuquan Iron & Steel (Group) Co., Ltd. invested in the project of the Raschel nickel-cobalt mine in Papua New Guinea. The project produces nickel hydroxide and cobalt hydroxide. The service life of the mine is 20 years. The annual output of products is 33,000 tons of nickel-containing metal and 3,300 tons of cobalt metal.

(4) Huayou Cobalt Industry (stock code: 603799.SH)

The company is a high-tech enterprise specializing in the deep processing of cobalt and copper non-ferrous metal smelting and new cobalt material products. The products are mainly used for lithium ion battery cathode materials, aerospace high-temperature alloys, hard alloys, color glazes, magnetic materials, rubber adhesives. Mixtures and petrochemical catalysts and other fields. The company is the largest producer of cobalt chemicals in China. It ranks second in China in terms of integrated production capacity of cobalt and is one of the largest in the world.

(5) Nickel sulfate

Nickel sulfate is mainly used in both battery and electroplating industries. In the battery industry, nickel sulfate is mainly used to produce ternary precursors. The main role of nickel in this industry is to increase the energy density of ternary materials. Under the trend of power batteries increasing energy density, the high nickelization of ternary materials will be the general direction, and the demand for nickel sulfate for high nickel systems will increase exponentially. According to calculations, theoretically, the demand for nickel sulfate for single ton NCM 111, 532, 622, 811 and NCA is 0.91, 1.36, 1.63, 2.16 and 2.19 tons. The demand for high nickel ternary nickel sulphate is low nickel ternary Around.

Figure: The amount of nickel sulfate required for different types of ternary cathode materials (tons)

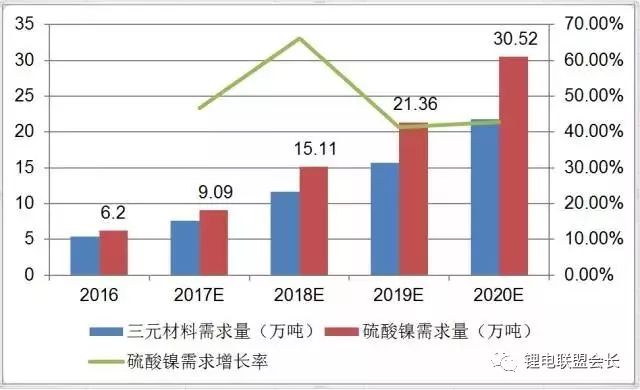

According to Asian Metals, the total domestic nickel sulfate production in 2016 was 247,000 tons, an increase of 32.4% year-on-year. In the first half of 2017, China’s cumulative production of nickel sulfate was 133,300 tons, an increase of 13% year-on-year. Due to the strong demand for downstream ternary materials, several domestic companies have plans to increase production. The nickel sulphate production capacity in 2017 is expected to exceed 350,000 tons and the production capacity in 2018 is expected to reach 470,000 tons. According to the domestic new energy automobile policy plan, domestic demand for ternary anode materials in 17-19 is expected to be 76,100 tons, 119,600 tons and 157,400 tons, respectively, a compound growth rate of 44%; benefiting from the rapid increase in the proportion of high nickel. The corresponding demand for battery-grade nickel sulfate was 90,900 tons, 151,100 tons and 2,136 tons, respectively. It is expected that the nickel sulfate production capacity can completely cover the supply demand in the short term, but taking into account the use of hydrometallurgical technology for the production of nickel sulfate, it is a highly polluting industry. Under the current situation where the domestic environmental protection policy is tightening, it may affect the operating rate of the manufacturers, resulting in Supply far less than capacity, it may also cause a gap between supply and demand.

Figure: Expected demand for nickel sulfate 2016-2020

Chart: Price Trend of Nickel Sulfate 2014

Major manufacturers:

Greene, China Metallurgical, and Platinum Institute.

IV Analysis of laws and regulations and industrial policies

Administrative authorities: Government Supervision The Ministry of Industry and Information Technology is the competent authority for the lithium ion battery industry in China. It is responsible for proposing new types of industrialization development strategies and policies, coordinating major issues in the process of new industrialization, and formulating and organizing the implementation of industry, communications, and information. Development plan, promote strategic adjustment and optimization of industrial structure, promote the integration of informatization and industrialization; formulate and organize the implementation of industrial, communications industry industry planning, plans and industrial policies; propose policy proposals for optimizing industrial layout and structure; and drafting Draft relevant laws and regulations, formulate regulations, formulate industry technical specifications and standards, and organize implementation to guide industry quality management; formulate and organize the implementation of energy conservation and comprehensive utilization of resources and cleaner production promotion policies in the industrial and communications industries; participate in the formulation of energy conservation and Comprehensive utilization of resources, clean production promotion planning, organization and coordination of related major demonstration projects and the promotion and application of new products, new technologies, new equipment, and new materials.

Industry management: The industry associations mainly include China Chemical and Physical Power Supply Association and China Battery Industry Association.

The China Chemical and Physical Power Industry Association is a national first-level association registered by the Ministry of Civil Affairs of the People's Republic of China and the competent department is the Ministry of Industry and Information Technology. The association was established in December 1989 and currently has more than 300 member units. It consists of six branches: alkaline storage battery and new chemical power supply branch, acid battery branch, lithium battery branch, solar photovoltaic branch, dry battery working committee and power accessories branch. mechanism.

The China Battery Industry Association was established in 1988 and has been registered and approved by the Ministry of Civil Affairs. It has the status of a legal person and is a national first-level association that spans regional, inter-departmental, and cross-ownership systems. The competent authority of the China Battery Industry Association is the State-owned Assets Supervision and Administration Committee, which also accepts the management of the Ministry of Civil Affairs and the China Light Industry Council.

The main policies in the industry are as follows:

List of major listed companies involved in the five industries

Flat Twin Cables

they are suitable for power & lighting circuits and building wiring. Also suitable for use as an earth wire the internal wiring of appliances and apparatus.

- Standard applied: BS 6004

- U0/U: 300/500V

- Certification: Third party test reports available

- Flame retardant or fire resistance or Low smoking and Halogen free or other property can be available

Flat Twin Cables,Flat Twin Wires,Outdoor Electrical Cable Types,Twin Flat Flexible Cable

Shenzhen Bendakang Cables Holding Co., Ltd , https://www.bdkcables.com